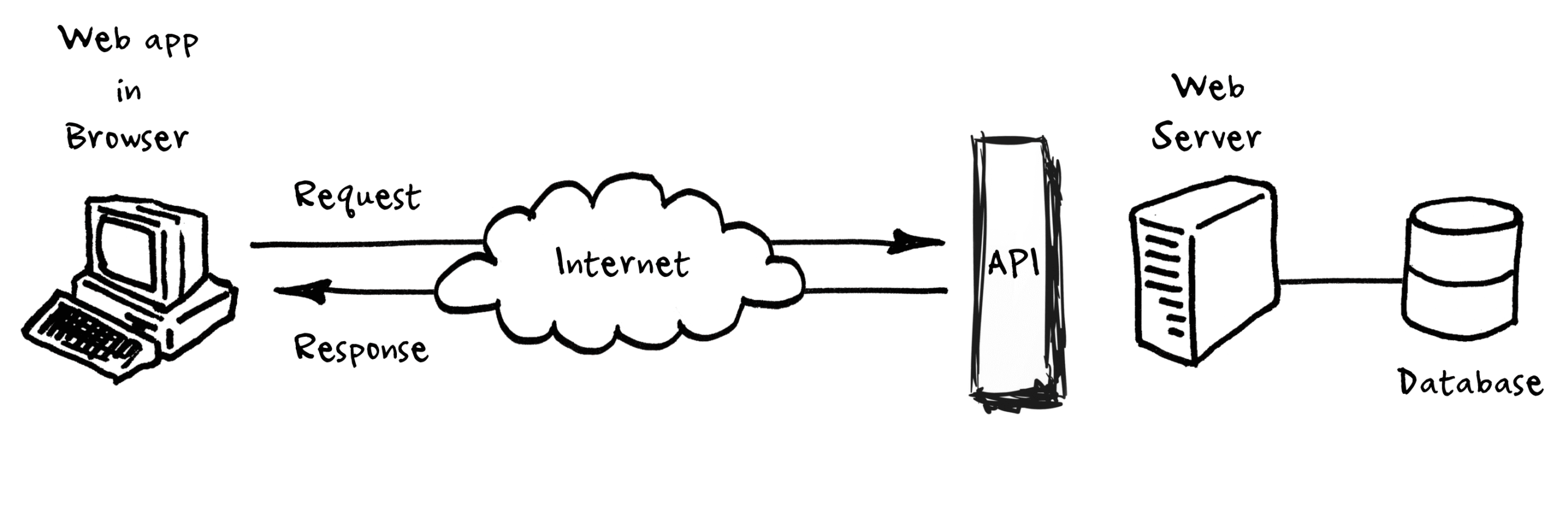

Financial services run on the rocket fuel of the APIs , their service innovation and value creation, being cost effective way to create the ecosystems ultimately In which the banks and the fintechs can be equal partners. Salesforce was launched at the IDG Demo 2000 conference almost 20 years ago. While the APIs are there from the time of the computers but it took the Salesforce to appreciate the critical value APIs brought to the banking system. It was Salesforce who shined light on how giving the access to the technology the innovation would be stimulated. And with the stimulated innovation subsequent rewards would be benefiting all the ones involved. This strategy was followed by many tech industry including eBay , Facebook and Amazon. Now there is similar epiphany seen in the banking systems again, the one that will have consequences much worse. It is pivoting financial services away from its home on Wall Street towards silicon valley since the banks have started vigorously using the APIs to access the technology in order to truly transform the experience they can give to their customers and the rewards they can share with investors. Banks have spent a fortune on the army of the in house developers to the write best software which can solve their problems. But so do their rivals, as even the competitive banks are also in the verge of software enhancement in order to solve the same issues including meeting changing customer demands and complying with new regulations – duplicating efforts and wasting time and money. This makes the banks struggle to compete with the challenger banks and also the platform companies which are seeming to be increasingly gulping on their space.

On the other hand, regulators who have pushed for the open banking system and the customers’ fast changing demands being fed by these possible digital age have themselves being caught up in between the traditional banks to innovate faster and to collaborate with the third parties. Embracing the APIs has given the banks a whole new access to the technology driven fintechs like artificial intelligence in fraud mitigation or credit card decision making technology that helps create value and all of these on a software-as-a-service (SaaS) basis. No one would like to change the engine while the plane is flying , and the fears over security and banks being embedded into their legacy IT mainframes are to blame. But the APIs now are safe and secure , lightweight and easy to understand. Developers comply with 3:30:3 rule: 3 seconds to understand what the API does; 30 seconds to identify the entry point and how it is used; and less than 3 minutes to create an account on the portal, gain access and start using the API. Which does not need any manual or special instructions to implement them and grant the access, the portals allows them to conduct mock tests and get them up and running in no time.

Before the decade is out, ecosystems of partners will be the norm and banks will no longer be the lynchpin. The lifestyle banking where financial services are embedded into customers’ lives exactly where they are needed such as point-of-sale loans or instant overdrafts will be the result. Banks might have become tech companies and SME services will be like a widget more than being a bank. By 2030, banks with their ecosystem partners will be able to adapt in minutes or hours and all thanks to the API.